%20(18).jpg)

At AIRINC, we love data. It drives the insights we share with our clients and fuels the tools we build to make global mobility easier.

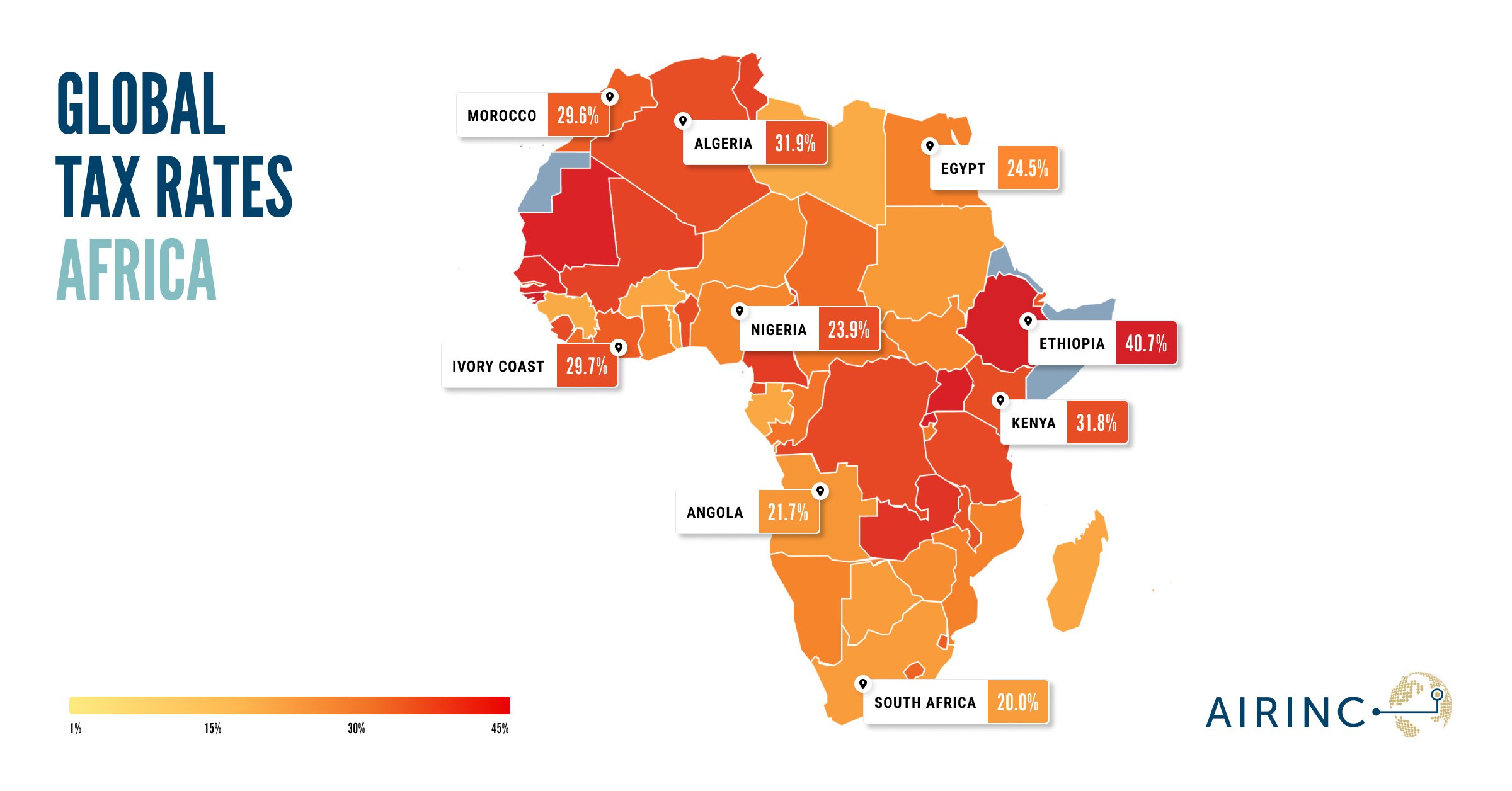

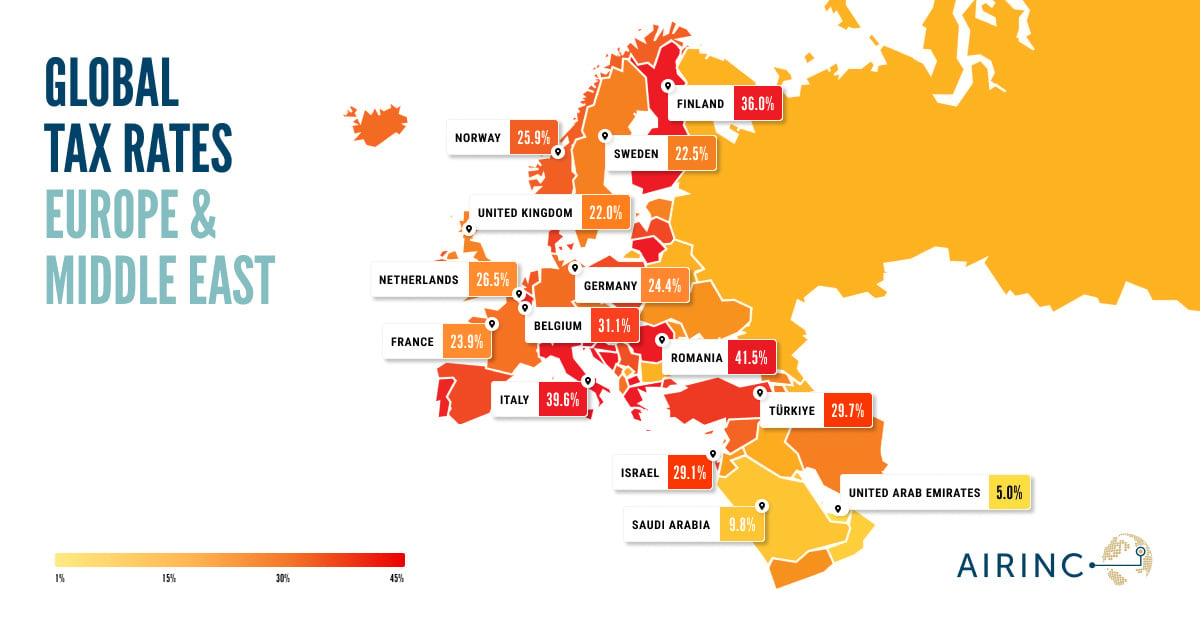

One of our most popular resources, the Global Tax Rates map, has just been updated with the latest 2026 data.

In 2026, several countries saw meaningful changes in effective tax rates due to updates to tax brackets, allowances, social security contributions, and family-related tax treatment. AIRINC’s updated Global Tax Rates map helps mobility teams compare how these changes affect take-home pay across countries and assignment locations.

This interactive tool helps you explore how taxes affect take-home pay in countries around the world. Whether you’re a mobility professional planning expatriate packages or simply curious about global tax systems, the map provides a clear, visual way to compare locations.

For the blog this year, we also looked at whether a taxpayer’s family size makes a difference in take-home pay.

Which Countries Had the Biggest Tax Rate Changes in 2026?

The world of taxes is always changing, and this year’s update includes some notable shifts. The largest effective tax rate decreases in this year’s update include Vietnam, Equatorial Guinea, and Zimbabwe. The largest increases include Azerbaijan, Rwanda, and Burundi.

Country, net change in the effective tax rate since last year

Azerbaijan: Up 6.44%

The beneficial regime introduced in 2019 for taxing employment income in the private sector, excluding employees in the oil and gas sector, expired on December 31, 2025. A new tax rate schedule has been introduced, with gradual increases also scheduled for 2027 and 2028. The social security formula has also been adjusted. The net effect is an increase in tax and a small decrease in social security for most taxpayers.

Burundi: Up 3.96%

The tax rate schedule has been adjusted. The net effect is an increase in tax for all taxpayers.

Equatorial Guinea: Down 7.09%

The tax rate schedule has been adjusted, with the top marginal rate reduced from 35% to 25%. The net effect is a decrease in income tax and a small increase in social security for all taxpayers, as the Worker Protection Fund is calculated based on after-tax income.

Rwanda: Up 5.01%

Normative deductions have been eliminated and social security rates have increased. The tax rate schedule is unchanged. The net effect is an increase in tax and social security for all taxpayers.

The government has introduced higher contribution rates to the pension scheme that will be implemented over a five-year period. Currently, the total combined employee contribution rate increases from 10.8% to 14.3% of wages without limitation. The combined employer rate increases from 12.8% to 15.8% of wages without limitation. These rates are scheduled to gradually increase over the next five years, resulting in an additional 4% for both employees and employers as of January 1, 2030.

Vietnam: Down 8.52%

The maximum contribution to unemployment insurance has increased slightly. Personal allowances have increased, and the tax rate schedule has been favorably adjusted. The net effect is a small increase in social security and a decrease in income tax for most taxpayers.

Zimbabwe: Down 6.56%

The Zimbabwe Revenue Authority has implemented adjustments to the tax brackets and the maximum contribution to social security. The annual maximum contribution for social security has increased from ZWG 5,034 to ZWG 7,179. The net effect is a decrease in income tax for all taxpayers and an increase in social security at higher incomes.

How Does Family Size Affect Take-Home Pay?

Some countries provide notable tax breaks for families with dependent children. For this comparison, we looked at the difference in 2026 tax rates and take-home pay between a single taxpayer and a married taxpayer with a nonworking spouse and two children.

For global mobility teams, family size can materially affect assignment cost projections because tax treatment may vary depending on marital status, dependent children, credits, allowances, or income-splitting rules.

Country, net savings in the effective tax rate for a family of four compared to a single taxpayer

Germany: 15.14%

Married taxpayers pay lower taxes than single taxpayers, as the income for a married couple is divided by two to calculate the separate tax, and the two tax amounts are then summed to determine the couple’s combined tax. Therefore, a couple with a nonworking spouse receives the benefit of the lower tax rates twice. Families with children also pay lower taxes due to a family allowance or child deduction, and lower social security contribution rates for disability and old-age insurance.

Luxembourg: 12.95%

Married taxpayers are allowed to split their combined income to take full advantage of the lower tax brackets twice. The limitations applied to certain deductions are based on family size, with larger families entitled to claim larger deductions.

Poland: 10.28%

Tax rates do not differ based on marital status. However, taxes can be reduced based on tax credits available for dependent children. Additionally, an election to file jointly with a spouse is possible when the couple has been married for part of the tax year. This allows the combined income to be split and the tax computed separately. This provides an advantage for couples with nonworking spouses, as income splitting allows the application of the lower tax brackets for both spouses.

Geneva, Switzerland: 10.58%

Married taxpayers pay taxes at lower rates than single taxpayers, and larger families may claim additional dependent allowances. In a referendum held on March 8, 2026, Swiss voters approved the abolition of the joint assessment of spouses and registered partners of the same sex. Consequently, each taxpayer shall be taxed on an individual basis. It is expected that the revision will enter into force on January 1, 2032.

California, United States: 10.82%

Different tax brackets apply based on marital status. Generally, the most favorable filing status is Married Filing Jointly. Taxpayers with qualifying children under age 17 may claim a USD 2,200 Child Tax Credit per child. The credit is phased out at higher income thresholds that vary by filing status.

Why This Matters

These updates are more than just numbers. For global mobility teams, tax changes affect cost projections, assignment budgets, and employee satisfaction. Staying informed helps you design competitive packages and avoid surprises.

Explore the Updated Map

The interactive map now reflects 2026 rates. Explore AIRINC’s updated Global Tax Rates map to compare 2026 tax rates, effective tax changes, and take-home pay across countries.

Frequently Asked Tax Questions

What are effective tax rates?

Effective tax rates show the overall tax burden on income after applying relevant tax rates, allowances, deductions, credits, and social security contributions. They help employers compare the real impact of tax systems on take-home pay across locations.

Why do global tax rates matter for mobility programs?

Global tax rates affect assignment cost projections, tax equalization calculations, compensation planning, and employee take-home pay. When tax rules change, mobility teams may need to review assignment budgets and employee communications.

Does family size affect take-home pay?

Yes. In some countries, marital status, dependent children, family allowances, child tax credits, or income-splitting rules can significantly affect take-home pay.